Essential Real Estate Closing Checklist for Buyers & Sellers

- Introduction

- Buyer Closing Documents

- Documents to Bring: Buyers

- Documents You'll Sign at Closing: Buyers

- Seller Documents & Final Verifications

- Documents to Bring: Sellers

- Critical Verifications Before Signing

- Understanding the Closing Disclosure

- Documents Buyers Sign at the Table

- Documents Sellers Sign and Provide

- What Can Go Wrong and How to Catch It

- Documents for Special Situations

- Using Technology to Stay Organized

- How to Prepare the Week Before Closing

- Final Thoughts

Introduction

Closing day may feel like the finish line, but it’s the most document-heavy part of buying a home. You’ll sign your name dozens of times, initial pages, review numbers, and somehow stay alert through a stack of papers that can easily top 100 pages. The average real estate closing involves signing 30 to 50 different documents in a single sitting. Missing an error or proof of insurance can delay the closing or result in signing away unintended rights.

This checklist guides you through document requirements and verifications before closing.

Real Estate Closing Process Overview:

Copy this checklist and paste it into Revdoku’s Generate Checklist to review your documents automatically:

Real Estate Closing Checklist for Buyers & Sellers

You are a real estate professional reviewing property transaction documents for completeness and legal accuracy. Check each requirement independently and flag every issue.

- Government-issued photo ID for all buyers listed on the mortgage

- Proof of homeowner's insurance (binder or full policy with effective date matching closing)

- Cashier's check or wire transfer confirmation for down payment and closing costs

- Wire transfer amount verified with closing agent 2-3 days before (never wire based solely on email)

- Loan commitment letter from your lender

- Recent pay stubs (within 30 days) if lender requested updated proof of employment

- Recent bank statements showing sufficient funds for closing

- Copy of home inspection report (for reference)

- Copy of appraisal report

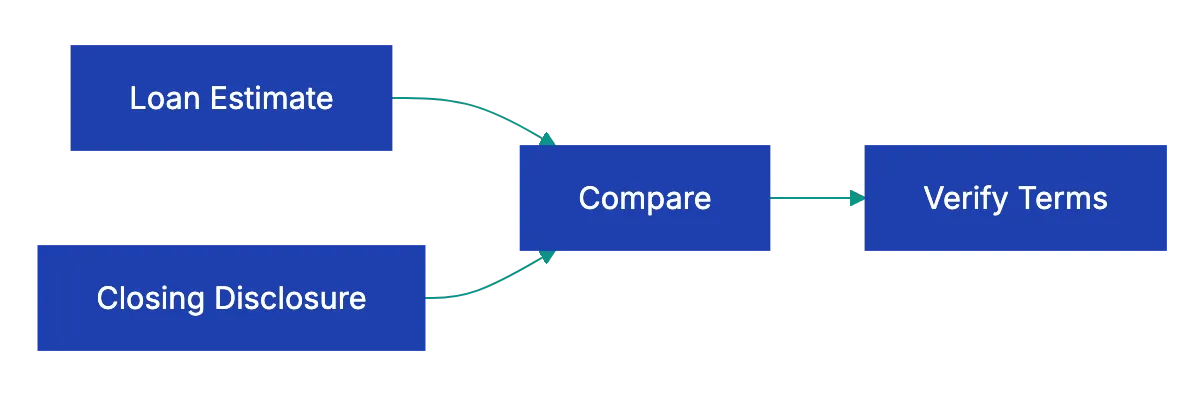

- Closing Disclosure reviewed line-by-line against your Loan Estimate

- Promissory Note with correct loan amount, interest rate, term, and monthly payment

- Deed of Trust or Mortgage creating lender's lien on property

- Warranty Deed or Grant Deed transferring ownership to you

- Title insurance policy (owner's policy)

- Escrow agreement for property taxes and insurance

- Occupancy affidavit stating whether property will be primary residence

- Identity affidavit confirming your legal name and any aliases

- Transfer tax declarations (required in most states)

- HOA documents if applicable (CC&Rs, budget, bylaws, meeting minutes)

- Government-issued photo ID for all sellers on the deed

- Signed and notarized deed prepared by closing agent or attorney

- Bill of sale for included personal property (appliances, fixtures)

- Affidavit of title stating no undisclosed liens or boundary disputes

- Mortgage payoff statement from your lender

- Lead paint disclosure for homes built before 1978

- Seller's property disclosure statement

- All keys, garage door openers, gate remotes, security system codes

- Manuals and warranties for appliances, HVAC, roof, or other systems

- All names spelled exactly as they appear on government ID

- Property address and legal description match deed and title documents

- Loan interest rate, term, and monthly payment match commitment letter

- Closing costs within $100 of the Closing Disclosure received 3 days prior

- Property tax proration calculated correctly based on closing date

- HOA dues prorated if applicable

- Seller credits for repairs or closing costs reflected in final numbers

- No prepayment penalty or confirmation it matches loan terms discussed

- Title insurance coverage amount equals purchase price

- Earnest money deposit credited toward your cash to closeBuyer Document Verification Flow:

Understanding the Closing Disclosure

The Closing Disclosure replaced the old HUD-1 settlement statement in 2015, and it’s the single most important document you’ll review before closing day. Federal law requires lenders to provide it at least three days before closing.

Use those three days to compare it against the Loan Estimate.

Start with page one. Your loan amount, interest rate, monthly principal and interest payment, and estimated taxes and insurance should match what you expected. If your interest rate changed, ask your lender for an explanation. If your monthly payment jumped by more than a few dollars, ask why before you proceed.

Page two of the real estate closing checklist breaks down closing costs. The current form replaced the older HUD-1 settlement statement. Lender fees, title fees, prepaid interest, homeowner’s insurance, property taxes, and HOA dues all get their own lines. Compare these figures carefully against page two of your Loan Estimate as part of your real estate closing document checklist.

Some fees cannot increase at all, like your lender’s origination charge. Others can increase up to 10 percent total. And some, like homeowner’s insurance you shopped for yourself, can increase without limit. But if your title insurance suddenly costs $500 more than estimated with no explanation, that’s a red flag worth questioning.

Page three shows the math for cash to close, including your down payment and any credits. A common error in the real estate closing checklist: the earnest money wired to the escrow company weeks ago doesn’t appear as a credit. Another: the seller agreed to pay $3,000 toward your closing costs, but it’s not reflected. Catch these problems during your three-day review period, not at the closing table.

Documents Buyers Sign at the Table

The promissory note is your promise to repay and includes loan terms. Read the prepayment section. Some loans charge a penalty if you pay off the mortgage early. If you didn’t agree to a prepayment penalty, don’t sign a note that includes one.

The deed of trust or mortgage gives the lender a security interest in your property. If payments stop, the lender can foreclose. The legal property description appears here, often written as metes and bounds or lot and block numbers that mean nothing to you. Ensure the street address and name are correct.

The deed transfers ownership from the seller to you. Your name as it appears on this deed becomes your legal ownership record. If your driver’s license says “Michael,” but you go by “Mike,” use Michael. If you’re married and taking title as joint tenants with rights of survivorship, the deed should say so. If you’re taking title as tenants in common with specified percentage ownership, that language belongs on the deed.

Once recorded, altering a deed involves filing a correction document and potentially re-signing loan documents, underscoring the importance of your real estate closing document checklist.

Title insurance comes in two policies: the lender’s policy and the owner’s policy. The lende’s policy proteccts the bank if sommeone cahllenges your ownership or discovers an old lien the title searc missed. You pay for it, but it protects the lender, not you. The owner’s policy protects you. In some states, sellers pay for the owner’s policy; in others, buyers pay. Either way, verify you’re receiving an owner’s policy with coverage equal to your purchase price.

Documents Sellers Sign and Provide

Sellers have fewer house closing documents, but the deed remains crucial. Sellers usually sign the deed before closing. The deed must be notarized. Some states require witnesss signatures in addition to notarization. If you’re selling property owned by a trust or LLC, the deed must be signed by the authorized trustee or member, and you’ll need to provide the trust document or operating agreement proving you have authority to sign.

The affidavit of title is a sworn statement that no liens, boundary disputes, easements, or claims exist against the property outside of what is disclosed in the house closing documents. Disclose if any boundary disputes exist. Disclose any secured debts. The title company can’t fijd what you don’t tell them about.

Your mortgage payoff statement shows the exact amount needed to pay off your existing loan as of closing day. Mortgage interes accrues daily, so the payoff amount increases each day. The closing agent will wire your payoff amount to your lender, and any remaining sale proceeds get wired to you. If your payoff is $182,456 but you thought you owed $180,000, ask your lender for a breakdown. You might owe interest from your last payment date to closing, a prepayment penalty, or a loan payoff fee.

What Can Go Wrong and How to Catch It

A 2019 study by the Consumer Financial Protection Bureau found that 30 percent of Closing Disclosures contained at least one error when firts delivered. Some errors are minor: a misspelled name, a wrong digit in the prpoerty tax account number. Others cos real money.

In one case, a buyer’s Loan Estimate showed the sellre paying $4,000 toward closing costs. The Closing Disclosure showed zero seller credits. The buyer caught it during the thre-day review and the erorr was corrected, but if he’d waited until closin day, the pressuure to porceed might have pushe him to absorb the cost rather than dealy.

Another comomn problem: property tax proration errors. If you close on July 15 and property taxes are paid in arrears, the seller owes you a credit for the taxes from January 1 through July 14. If the closing agen uses the wrong daily rate or miscounts the days, you could overpay by hundreds of dollars. Bring a calculator. Verify the math.

Wire fraud is risong. In 2022, the FBI reported that real estaet wide fraud cost buyers $396 million. Here’s the scheme: a scammer impersonating your closing agent or title company sends an email with wiring instructions. You wirre yuor down payment to the fraudulent account. By the time you arrive at closing and find the money never arrived, it’s gone.

Protect yourself with one simple rule: never wire money based on emmailed instructions. Call your closin agent at a number you looked up yourself, not one included in the email. Verify the account number, routing number, and recipient name oveer the phone. Then send a test wire of $50 before wiring the full amount. Yes, this adds a day to the process. It also prevents losing your down payment to a criminal in another country.

Documents for Special Situations

If you’re buying a condo or a home in a planned community, expect an extra set of HOA documents. The association’s CC&Rs spell out rules about exterior paint colors, landscaping, parking, noise, and pet restrictions. The current budget shows monthly HOA dues and any special assessments plannned. Meeting minutes from the past six to twelve months reveal whethher the association is functional or mired in disputes.

Some lenders requier a questionnaire clmpleted by the HOA confirming the association is in good standimg, adequately insured, and has sufficient reserves.

If you’re buying a property with a well or septic ssytem, your lender may require a well water tes and septic inspection reporrt. These aren’t closing documents exactly, but you’ll need to provid them to satisfy lpan conditions. If the septic system failed inspection and the seller agreed to repair it, bring proof the repair was completed and the system passed re-inspection.

If you’re buying a property that’s part of an etsate sale, expect additional documentation. The executor must provide letters testamentary or letters of administration proving court authority to sell the property. If the estate is in probate, the court order approving the sale become part of the closing package. These sales often take longer to close because the executo must notify heirs and sometimes obttain courrt aprpoval for the sale price.

Using Technology to Stay Organized

Real esttate closings generate mountains of paper, but you don’t have to manage them manualyl. See 30 to 50 different documents. A documnet revview platform like Revdoku can help you sta organizrd from offer to closing. Upload your purchase agreement, inspection report, loan estimate, and closing disclosure. Build a workflow that checks each document against your closing requirements checklist.

For example, when your Closing Disclosure arrives, upload it and run an automated comparison against your Loan Estimate. Flag any line item that increased by more than the allowable tolerance. Check property tax calculation, verify earnest money credits, and confirm seller concessions appear. The platform can flag errors faster than manuallly comparign two multi-page forms line by line.

You can also use AI-powered tools to extract key terms from dense legal documents. Instead of reading forty pages of HOA CC&Rs to find the pet policy, let the AI summarize restrictions in plai language. Instead of deciphering the prepayment penalty clause in your promissory note, ask the tool to explain whether you’ll owe a fee if you refinance in two years.

This isn’t about replaciing your real estate attorney or closing agent. It’s abuot arriving at the closing tabl informed and confident instead of confused and rushe. When you’ve alread reviewed every document, verified the numbers, and flagged potential issues, closing day becomes a formality instead of a fire drill.

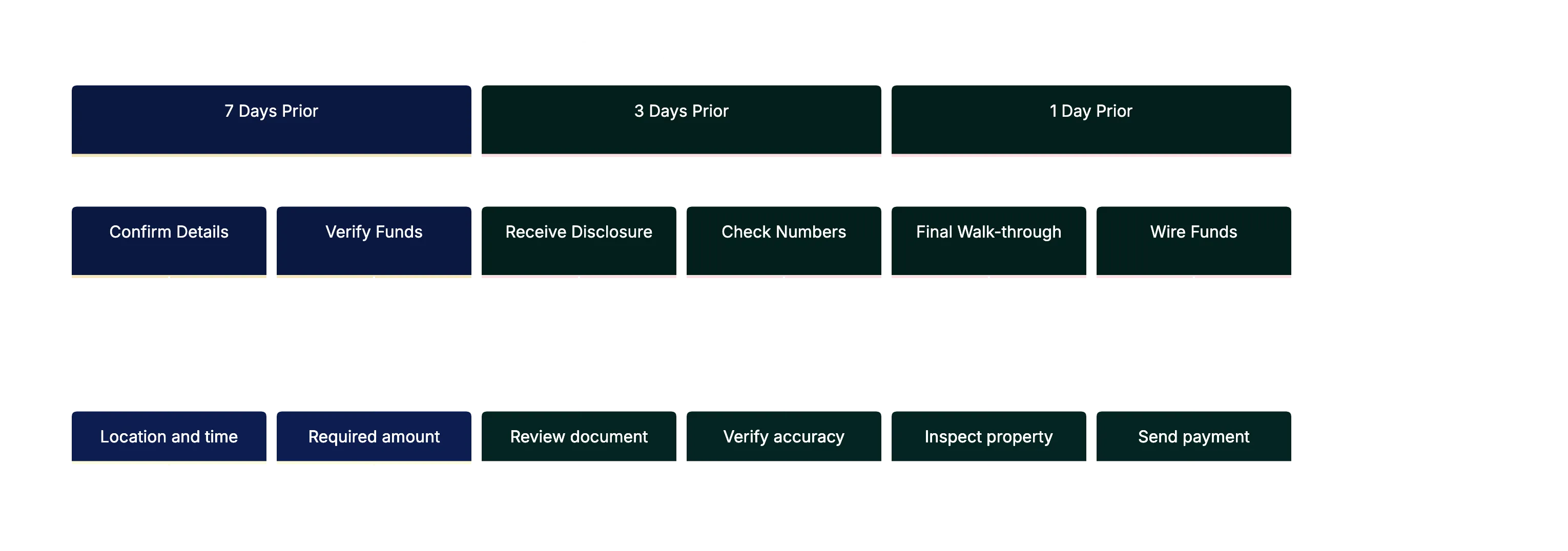

How to Prepare the Week Before Closing

- 7 days before: confirm closing date, time, and location. Ask how much you’ll owe and in what form — most agents require a cashiier’s chekc or wire transfer for amounts over $1,000. Personal checks usually aren’t accepted for large amounts.

- 3 days before: you should receive your Closing Disclosure. Review it immediately. If you spot an error, contact your lender right away — some corrections require reissuing the Closing Disclosure and restarting the three-day waiting period.

- 2 days before: do a final walk-through to verify the property is in the same condition as when you made your offer and that agreed repairs are complete. Turn on faucets, flush toilets, and test garage doors.

- 1 day before: gather your documents — ID, insurance binder, cashier’s check or wire confirmation, and copies of reports. If wiring funds, send the wire first thing in the morning so it clears before closing.

Final Thoughts

Closing on a house involves more paperwork than almost any other transaction you’ll complete in your lifetime. The real estate closing document checklist above covers the standard documents, but your specific closing may include additional paperwork depending on your state, loan type, and property type. Stay organized, verify everything, and don’t be afraid to pause and ask questions during the signing.

Pre-Closing Timeline:

Remember, the closing agent isn’t your adversary. Their job is to make sure a clean transaction where both parties understand what they’re signing. If a document doesn’t match what you expected or includes terms you didn’t agree to, say so. Better to delay closing by a day to fix an error than to sign a mistake that costs you thousands or creates legal problems down the road. Use the checklist and upload documents to a review platform beforehand to make closing day smooth.

Find more review checklists at revdoku.com/checklists — each one is ready to copy and use in the app.

Frequently Asked Questions

What should I do if I notice an error in my Closing Disclosure?

If you find an error in your Closing Disclosure, contact your lender immediately. Some corrections may require reissuing the document, which can reset the mandatory three-day review period. It's essential to address these discrepancies before closing day to avoid delays or unexpected costs.

How can I verify the legitimacy of wire transfer instructions?

To ensure the safety of your wire transfer, never rely solely on emailed instructions. Always verify the account details by calling your closing agent at a phone number you obtained independently, not from the email. Consider sending a small test wire before transferring larger sums to minimize risk.

What types of documents should I prepare a week before closing?

One week before closing, confirm the closing date, time, and location. You should also prepare your government-issued ID, proof of homeowner's insurance, and funds for the down payment. It's best to review your Closing Disclosure immediately upon receipt to catch any discrepancies early on.

What happens if the seller's disclosure reveals issues after I close?

If the seller's disclosure reveals undisclosed issues post-closing, it may require legal action depending on the nature of the problem and state laws. Always review the seller's property disclosure statement carefully before closing, and consider having it evaluated by a real estate attorney if needed.

Can I use technology to help with the closing process?

Yes, technology can significantly streamline the closing process. Document review platforms like Revdoku allow you to organize paperwork, compare documents, and flag discrepancies efficiently. Additionally, AI tools can help summarize lengthy legal documents for easier understanding.

What should I focus on during the final walk-through?

During your final walk-through, check that the property is in the same condition as when you made your offer. Ensure that all agreed-upon repairs are complete, and test key systems like plumbing and electrical to confirm everything is functioning properly. This step is crucial to avoid surprises at closing.

What unique documents should I expect if buying a condo?

When purchasing a condo, you should expect to review additional documents including the homeowners association (HOA) documents, which detail restrictions, current budgets, and meeting minutes. Lenders may also require a questionnaire to confirm the HOA's financial stability and insurance coverage. Being informed about these documents can prevent future issues related to HOA rules and fees.